2024 Annual Review: US$1 Trillion in Buybacks Led by Apple, Meta, Nvidia

Apple Inc. AAPL | 253.11 | -0.97% |

Alphabet Inc. Class C GOOG | 193.40 | -0.33% |

Alphabet Inc. Class A GOOGL | 192.14 | -0.32% |

Meta Platforms META | 596.71 | -0.52% |

NVIDIA Corporation NVDA | 139.12 | +1.54% |

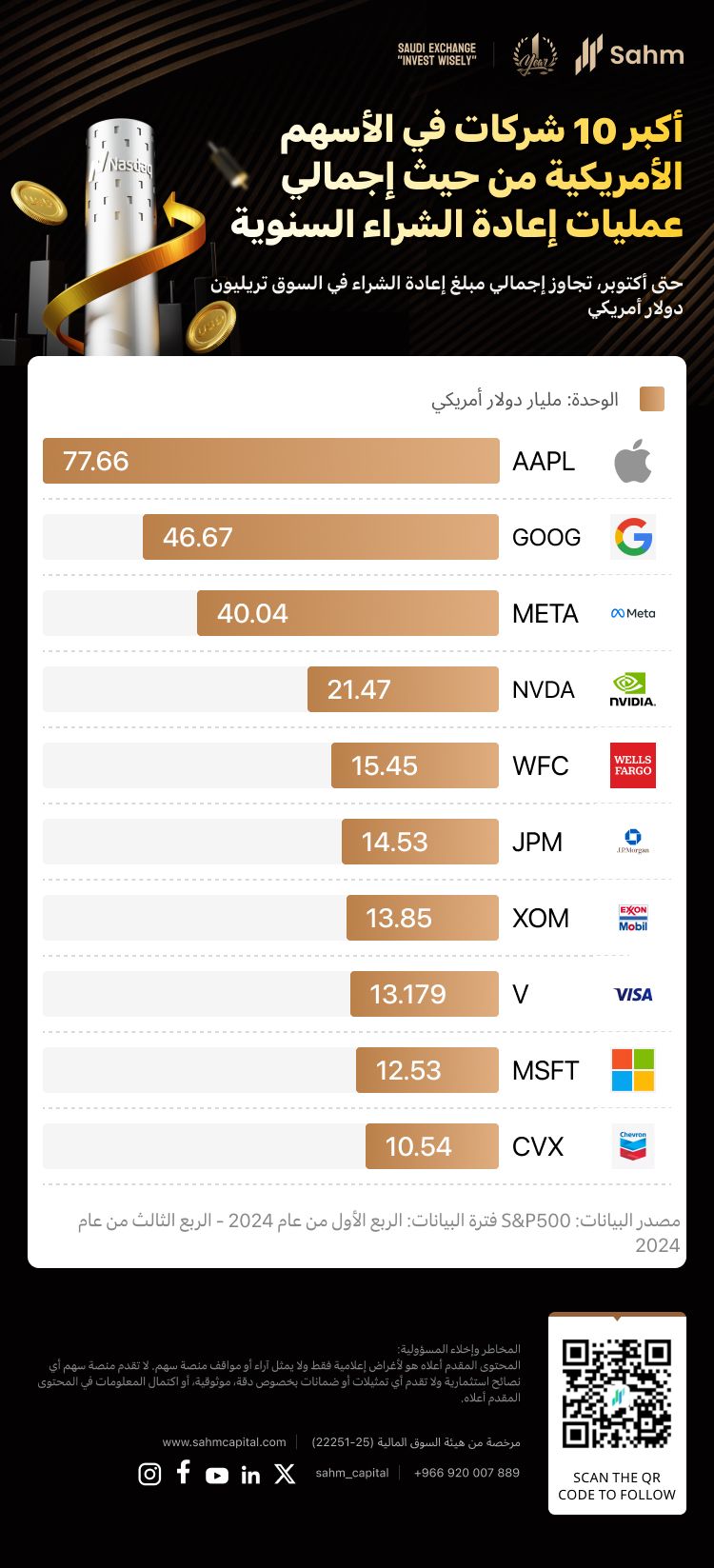

According to EPFR data, as of the third quarter, the total amount of share buybacks by companies across the entire U.S. stock market exceeded $1 trillion, set to break the historical record set in 2022. Among these, more than half of the buyback amounts were attributed to S&P 500 index constituents, with the buyback amount nearing $700 billion for the year.

S&P Global data shows that the buyback landscape of the U.S. stock market this year continues to be dominated by leading tech stocks, with financial and oil and gas stocks being the main forces. Apple Inc.(AAPL.US) tops the list with a cumulative buyback amount of $77.66 billion as of the third quarter, reflecting nearly a 27% increase from the previous year. Over the past five years, Apple has spent approximately $448 billion on buybacks, contributing significantly to its long-term stock price appreciation.

The second and third places in the U.S. stock market buyback rankings remain the same as last year, held by Alphabet ( Alphabet Inc. Class C(GOOG.US) Alphabet Inc. Class A(GOOGL.US) ) and Meta Platforms(META.US), respectively. Notably, Meta's buyback amount surged to $40 billion this year, more than doubling (115% increase) compared to last year. Meta’s stock has also performed exceptionally well, with a year-to-date increase of over 75%, leading among the seven tech giants.

Among tech giants, NVIDIA Corporation(NVDA.US) and Microsoft Corporation(MSFT.US) are also among the top ten in buyback volume. Benefiting from the explosion in AI demand, NVIDIA has accrued significant cash reserves, with a buyback amount of $21.4 billion in the first three quarters alone, more than double the amount from the same period last year. In August, NVIDIA's board further approved a $50 billion stock buyback plan.

According to Bank of America analysts, NVIDIA's free cash flow is expected to reach $200 billion or more over the next two years. Combined with its existing large cash reserves, NVIDIA is expected to have about $175 billion in surplus liquidity by early 2027, surpassing the current cash king, Apple. This potentially provides ample incentive for increased dividends and buybacks in the future for this AI leader.

Additionally, traditional buyback giants Wells Fargo & Company(WFC.US) and JPMorgan Chase & Co.(JPM.US) saw increases in their buyback amounts this year, both exceeding $10 billion.

Buybacks are a way for listed companies to provide returns to shareholders by purchasing stock and canceling shares, which increases earnings per share and boosts stock prices. Research indicates that buybacks and cash dividends are equivalent in terms of shareholder returns, but U.S. listed companies, especially in the tech sector, tend to favor buybacks.

In the long term, buybacks have become a significant driver of the U.S. stock market’s rise. Against the backdrop of a positive correlation between buyback scale and corporate earnings, rising earnings could propel increased buybacks, forming a positive cycle of "earnings improvement → increased buybacks → stock market rise."

Looking at the quarterly buyback scale of the S&P 500 index since 2007, there is a noticeable positive correlation between the buyback scale of S&P 500 constituents and the index's performance. Based on this year's performance, this trend appears to persist.

According to institutional analysis, there are generally two periods of high buyback activity: first, during the mid to late stages of interest rate hikes and peak interest rates, when the economy is booming, corporate profits are strong, and cash flow is abundant, leading to robust buybacks; and second, during periods of low interest rates and low financing costs, when corporate valuations are generally low, prompting strong incentives for debt-financed buybacks. With the arrival of an easing cycle, a new wave of buyback activity may emerge, presenting more opportunities for investors.