Dutch Bros (BROS) Nationwide Expansion Success: Is Customer Loyalty the True Engine of Long-Term Growth?

Dutch Bros BROS | 0.00 |

- Dutch Bros reported second-quarter results that surpassed analyst expectations on both earnings and revenue, while highlighting the company's rapid nationwide expansion with over 1,000 locations and plans to open 150 new shops this year.

- This expansion includes breaking into new states like Illinois and South Carolina and is supported by strong customer growth through digital and loyalty program initiatives amid competition from major coffee chains.

- We'll examine how the positive earnings surprise and rapid market expansion could influence Dutch Bros' long-term growth outlook.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Dutch Bros Investment Narrative Recap

To be a shareholder in Dutch Bros, you need to believe in its ability to translate rapid US expansion and digital engagement into sustained sales and profit growth, while managing the pressures of rising labor costs and stiff competition. The recent news of strong Q2 results and ambitious new market entries like Illinois and South Carolina directly supports optimism around near-term revenue momentum, but doesn't meaningfully alter the key short-term catalyst, preserving same-shop sales growth in the face of market saturation, and the biggest risk, which remains labor cost inflation.

Among the various company developments, Dutch Bros' raised revenue guidance to US$1.59–1.60 billion is the most relevant here, as it underpins the current growth trajectory reflected in this quarter’s earnings beat and rapid shop openings. This forward-looking signal gives investors a tangible metric to watch as the company executes its aggressive store rollout strategy, but also raises the stakes for maintaining build-out efficiency and margin discipline.

On the other hand, investors should be mindful of the potential downside from relentless wage pressures if new market sales fail to...

Dutch Bros' outlook targets $2.6 billion in revenue and $197.4 million in earnings by 2028. This scenario assumes a 21.8% annual revenue growth rate and a $140.2 million increase in earnings from the current level of $57.2 million.

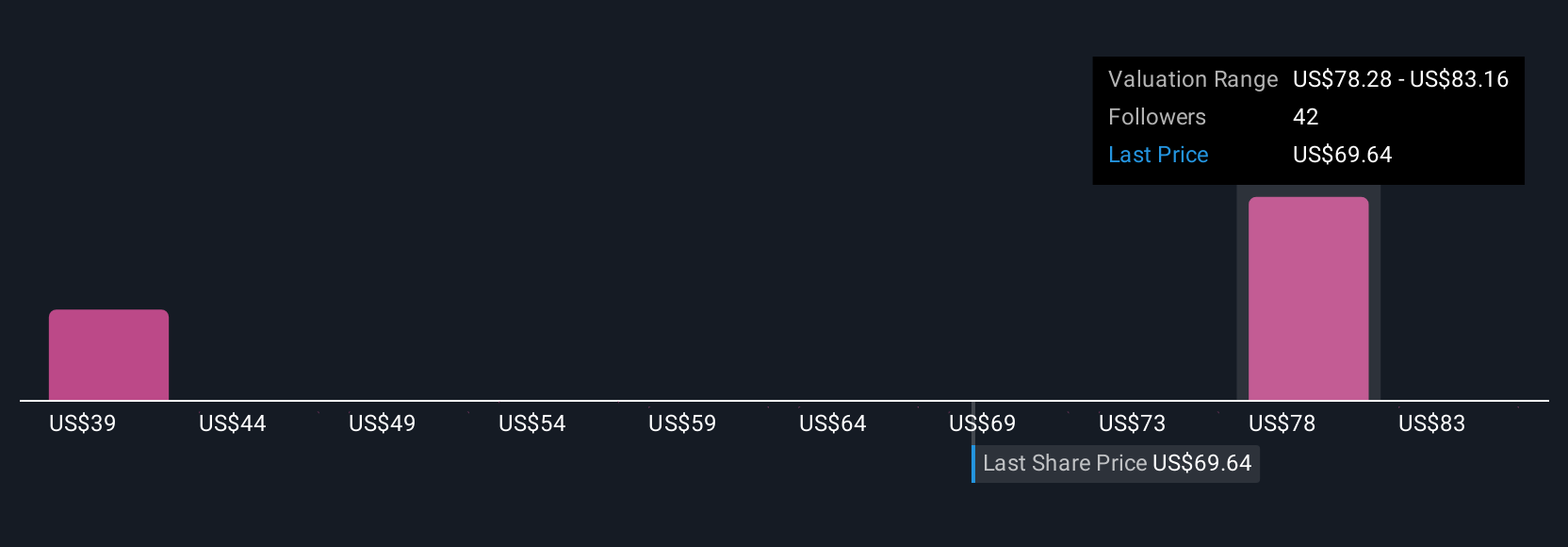

Uncover how Dutch Bros' forecasts yield a $82.62 fair value, a 50% upside to its current price.

Exploring Other Perspectives

Ten fair value estimates from the Simply Wall St Community span a wide range from US$44.11 to US$95.38 per share. Aggressive expansion remains a core catalyst, but it brings greater scrutiny to whether shop growth can consistently boost long-term earnings and margins, take a look at how different community members see it playing out.

Explore 10 other fair value estimates on Dutch Bros - why the stock might be worth as much as 73% more than the current price!

Build Your Own Dutch Bros Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Dutch Bros research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Dutch Bros research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Dutch Bros' overall financial health at a glance.

Seeking Other Investments?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Find companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.