Casella Waste Systems (NASDAQ:CWST) Has A Pretty Healthy Balance Sheet

Casella Waste Systems, Inc. Class A CWST | 106.42 | +0.17% |

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Casella Waste Systems, Inc. (NASDAQ:CWST) does carry debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

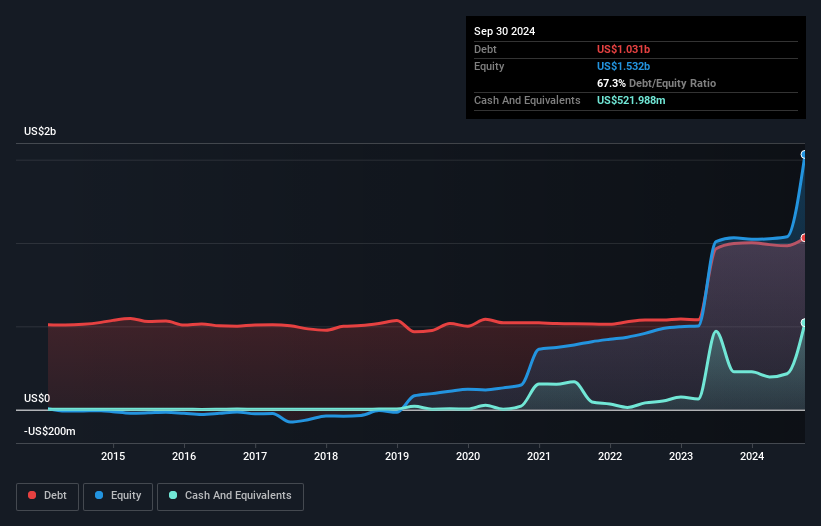

How Much Debt Does Casella Waste Systems Carry?

As you can see below, Casella Waste Systems had US$1.03b of debt, at September 2024, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of US$522.0m, its net debt is less, at about US$509.4m.

How Healthy Is Casella Waste Systems' Balance Sheet?

According to the last reported balance sheet, Casella Waste Systems had liabilities of US$291.3m due within 12 months, and liabilities of US$1.30b due beyond 12 months. Offsetting this, it had US$522.0m in cash and US$173.1m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$896.6m.

Of course, Casella Waste Systems has a market capitalization of US$7.06b, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While Casella Waste Systems has a quite reasonable net debt to EBITDA multiple of 1.6, its interest cover seems weak, at 1.9. The main reason for this is that it has such high depreciation and amortisation. While companies often boast that these charges are non-cash, most such businesses will therefore require ongoing investment (that is not expensed.) In any case, it's safe to say the company has meaningful debt. Sadly, Casella Waste Systems's EBIT actually dropped 3.2% in the last year. If that earnings trend continues then its debt load will grow heavy like the heart of a polar bear watching its sole cub. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Casella Waste Systems's ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Casella Waste Systems produced sturdy free cash flow equating to 72% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

Casella Waste Systems's interest cover was a real negative on this analysis, although the other factors we considered were considerably better. There's no doubt that its ability to to convert EBIT to free cash flow is pretty flash. Considering this range of data points, we think Casella Waste Systems is in a good position to manage its debt levels. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.